Neobanks and Challenger Banking

84

%

7.9

The only AI-powered strategic intelligence platform that transforms global market shifts into high-impact decisions for banking leaders navigating industry disruption.

Neobanks are building core banking systems in-house to enhance operational control and resilience. This shift towards self-reliance indicates a growing trend where digital banks prioritize agility and cost-effectiveness to compete with traditional banks, impacting their long-term independence positively.

The neobank trend underscores the pressing need for banks to modernize their operations, leveraging fintech advancements to improve customer engagement and streamline processes, directly impacting cost structures and enhancing service accessibility. As neobanks continue to scale globally, they catalyze intensified regulatory scrutiny which could compel traditional banks to revisit compliance strategies and adapt to shifting regulations across jurisdictions.

To enhance profitability and growth, your banking company could explore strategic partnerships with fintech firms to develop innovative digital financial products. This action can access technological expertise, improving customer satisfaction through diversified offerings and enhancing the digital banking experience, positioning the company for market expansion. Investing in scalable cloud-native infrastructure, similar to Mambu's strategy in providing banking solutions, will support the bank's digital transformation and operational efficiency.

AI agents are increasingly being integrated into financial systems, enhancing efficiency in transaction monitoring and compliance. They automate mundane tasks and allow banks to focus on strategic objectives, potentially elevating the efficiency and productivity of banking operations.

AI agents provide quick, automated payment processing, reducing manual entry errors and freeing up bank resources, encouraging banks to roll out AI-powered services for efficiency in core operations.AI-powered banking enhances customer service with faster payment responses and personalized interactions, influencing customer retention positively. Banks integrating AI agent solutions could face increased scrutiny and regulation as they navigate the challenges of data privacy and transactional security.

Invest in AI agent payment tools to enhance customer transaction experiences by integrating agentic AI for seamless, autonomous payments. This supports regulatory compliance, boosts customer satisfaction, and aligns with digital transformation goals. Political and technological factors converge here, impacting operational efficiency and innovation in services.

Data portability is transforming competition in the banking industry, enhancing user control and reducing barriers to switching financial service providers. This trend is fostering innovation, as institutions develop new services and improve customer engagement to retain and attract consumers.

Data portability facilitates easier switching between banks and financial products for consumers, potentially increasing competition and disloyalty to single institutions. This can lead to higher customer acquisition costs and more pressure to improve services. Over time, as customers gain more control over their data, the competitive differentiation will shift towards personalized banking experiences and innovative product offerings, increasing the need for banks to invest in technological solutions and customer relationship management

Data portability facilitates easier switching between banks and financial products for consumers, potentially increasing competition and disloyalty to single institutions. This can lead to higher customer acquisition costs and more pressure to improve services. Over time, as customers gain more control over their data, the competitive differentiation will shift towards personalized banking experiences and innovative product offerings, increasing the need for banks to invest in technological solutions and customer relationship management

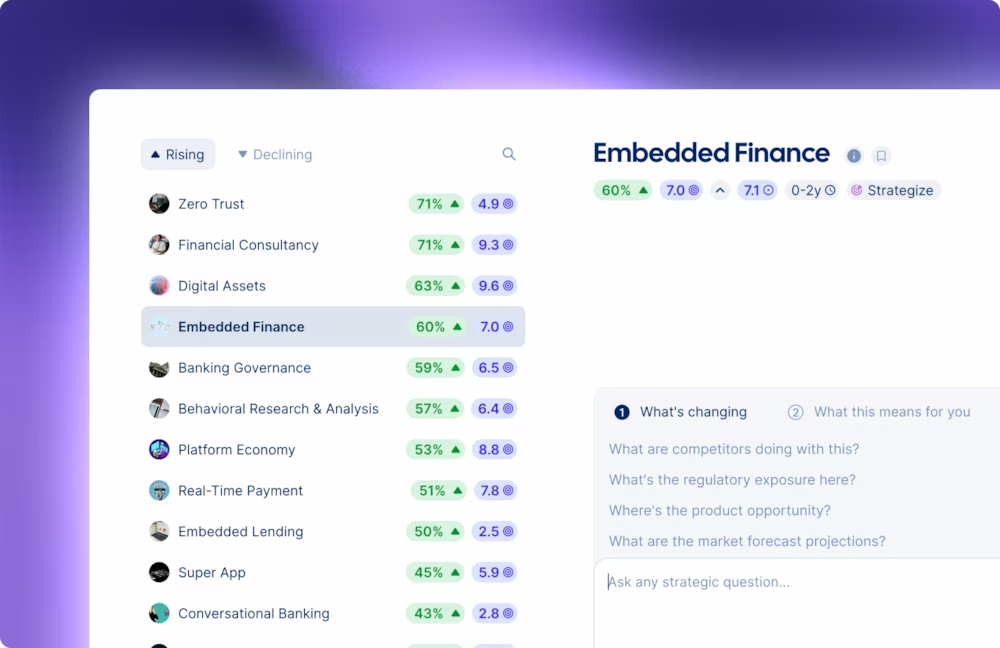

Trendtracker scores structural shifts across digital money, payment infrastructure, and financial regulation by Strength and Momentum - so teams can directly compare which changes are accelerating and which are still early. The result is a clear, continuously updated basis for deciding where to act, where to watch, and where to wait, before market pressure makes the choice for you.

Yes. Trendtracker tracks regulatory signals across geographies and surfaces emerging frameworks alongside the market and technology trends they intersect with, giving your risk and compliance teams early visibility into where regulation is heading, not just where it currently stands. This is particularly relevant for banks operating across multiple regulatory environments simultaneously.

Trendtracker tracks startup funding activity, emerging technology adoption, and new market entrants across banking-relevant domains. This makes it easier to spot potential partners, future competitors, and technology bets worth exploring early, rather than reacting once disruption is already underway.

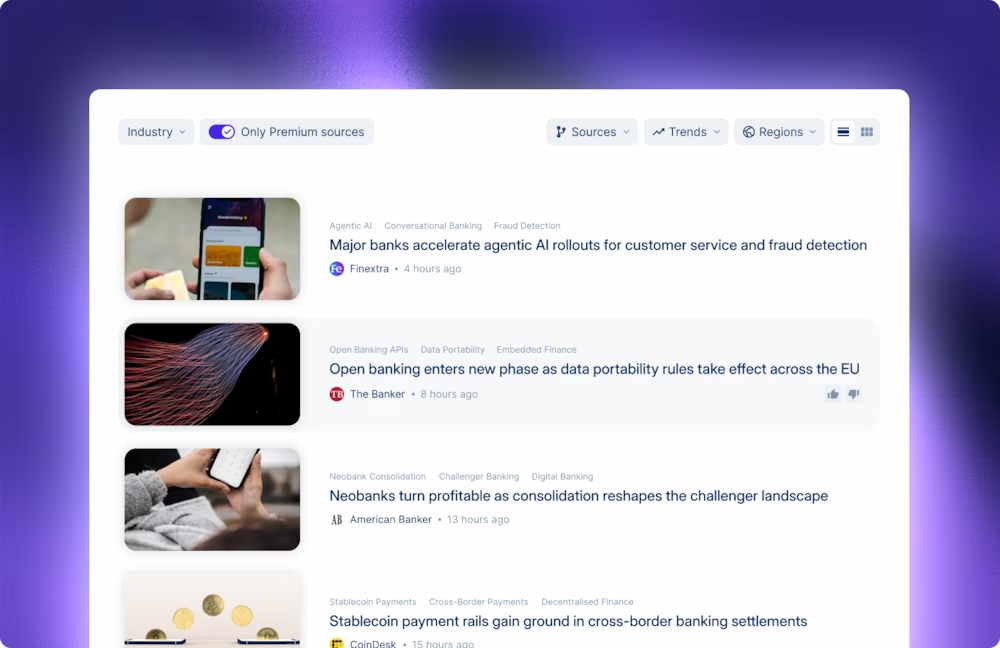

Trendtracker monitors {{sources}}+ sources across regulatory filings, scientific research, startup activity, industry news, and macroeconomic signals, different functions across the bank can each find what is relevant to their specific mandate (structural market shifts / regulatory developments / emerging technology), all from the same intelligence base, without each function needing separate tools or processes.

Trendtracker continuously monitors regulatory signals across geographies - scoring each by momentum so teams can distinguish between requirements that are hardening and those still under development. This gives risk and compliance teams early visibility into where regulatory pressure is building before it reaches the implementation stage, leaving time to assess the impact on products, operations, and capital allocation rather than reacting under deadline.

.avif)