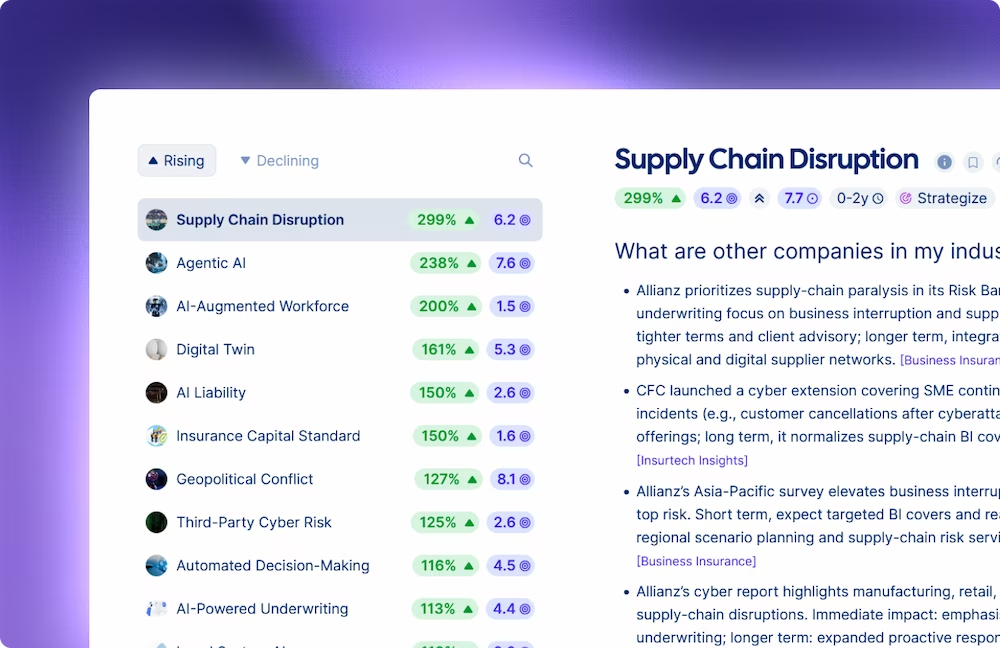

AI-Powered Underwriting

111

%

7.0

Trendtracker gives insurance strategy, risk, and foresight teams a continuous view of the signals reshaping your industry, so you're driving the conversation in the boardroom, not reacting to it.

AI-powered underwriting has seen increasing adoption in the insurance industry as companies aim to enhance decision-making speed and accuracy. This trend facilitates efficient data use and service delivery, potentially reshaping traditional underwriting methods. However, challenges like talent gaps and customer trust must be addressed long-term.

The trend of AI-powered underwriting leads to an initial impact on operations by speeding up data processing, allowing for faster decision-making, thereby improving customer experience by reducing underwriting times. AI adoption reduces operational costs but requires investment in advanced AI solutions and employee upskilling, impacting costs and talent development significantly.

Insurers can integrate modular AI underwriting solutions to enhance risk assessments, reduce costs, and improve decision-making efficiency. This approach aligns with trends in AI's practical applications and allows insurers to implement AI in stages, adapting to specific challenges such as climate volatility and rising cyber risks

AI-driven misinformation and deepfakes pose significant risks to the insurance industry by complicating trust and credibility. Insurers are increasingly vulnerable to fraudulent claims and identity theft, needing advanced technologies to bolster fraud detection and prevention systems.

The rise of AI-driven misinformation and deepfakes increases operating costs as insurers invest in advanced fraud detection technologies for claims and underwriting processes. Cyber insurance policies are adapting to include deepfake-driven risks, reshaping coverage options and requiring insurers to enhance policy transparency and clarity around AI-generated cybercrime.

To counter the increasing sophistication of AI-driven misinformation and deepfake fraud, insurers could invest in advanced AI detection tools. This strategic action enhances fraud detection and prevention, improving the authenticity of claims processing, thereby mitigating risks associated with fraudulent activities.

The global protection gap remains a significant issue for insurers as climate change impacts and natural disasters increase uninsured losses. The industry is pushed to innovate beyond traditional policies to address these evolving risks effectively.

The global protection gap trend has direct impacts on operational costs as insurers must adjust pricing models due to increasing uninsured risks. It also challenges insurers to innovate products and solutions to bridge gaps in coverage effectively

Invest in educational initiatives to address the life insurance protection gap, particularly among women and millennials, to increase trust and penetration rates. Targeted campaigns and partnerships with NGOs could address systemic biases and market challenges. This will aid in catering to underserved demographics, increasing customer equity and loyalty.

Yes. Teams across business lines and geographies each work within independently configured views tailored to their mandate, while drawing from the same intelligence base. Leadership maintains a single view across the organisation. This allows a property and casualty team in one region and a life insurance team in another to work simultaneously without overlapping their efforts.

Trendtracker supports the full intelligence cycle - signal detection, implication analysis, and evidence-backed briefing that are continuously updated, so detection-to-response time shrinks without the fragmented research process.

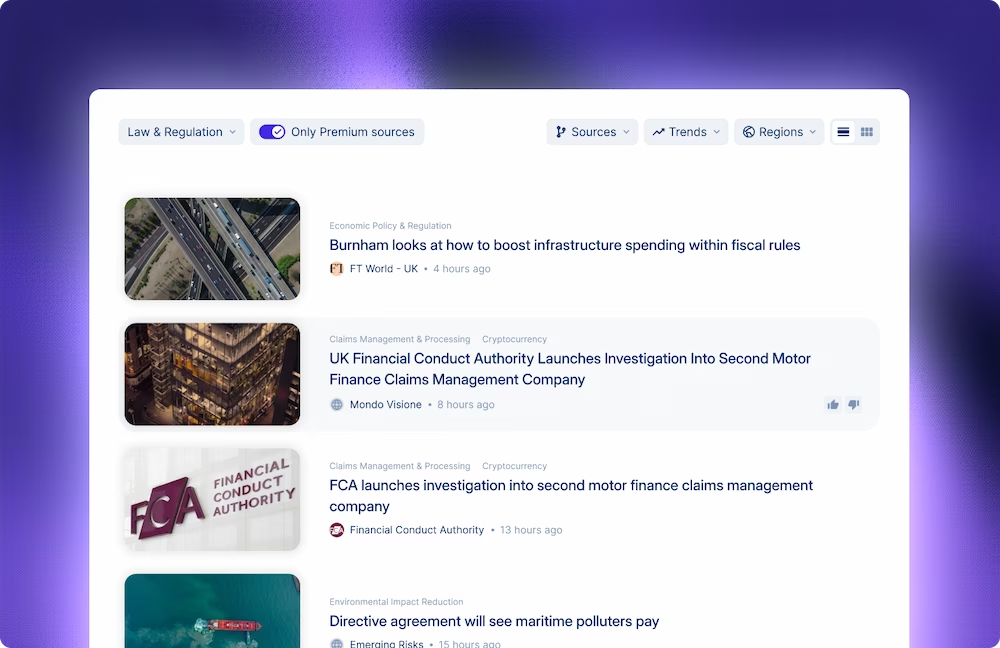

Trendtracker generates structured, evidence-backed briefings in minutes - drawing on {{sources}}+ curated sources including regulatory filings, scientific research, and investment data. Every insight is traceable to its original source, so teams walk into board discussions with a clear, defensible picture of what is moving and why.

Trendtracker is designed to sit alongside existing intelligence sources, not replace them. Where analyst reports provide depth on specific topics at a point in time, Trendtracker provides continuous, cross-domain signal monitoring that surfaces what is moving between those reports, scoring which signals are gaining enough momentum to warrant deeper attention.

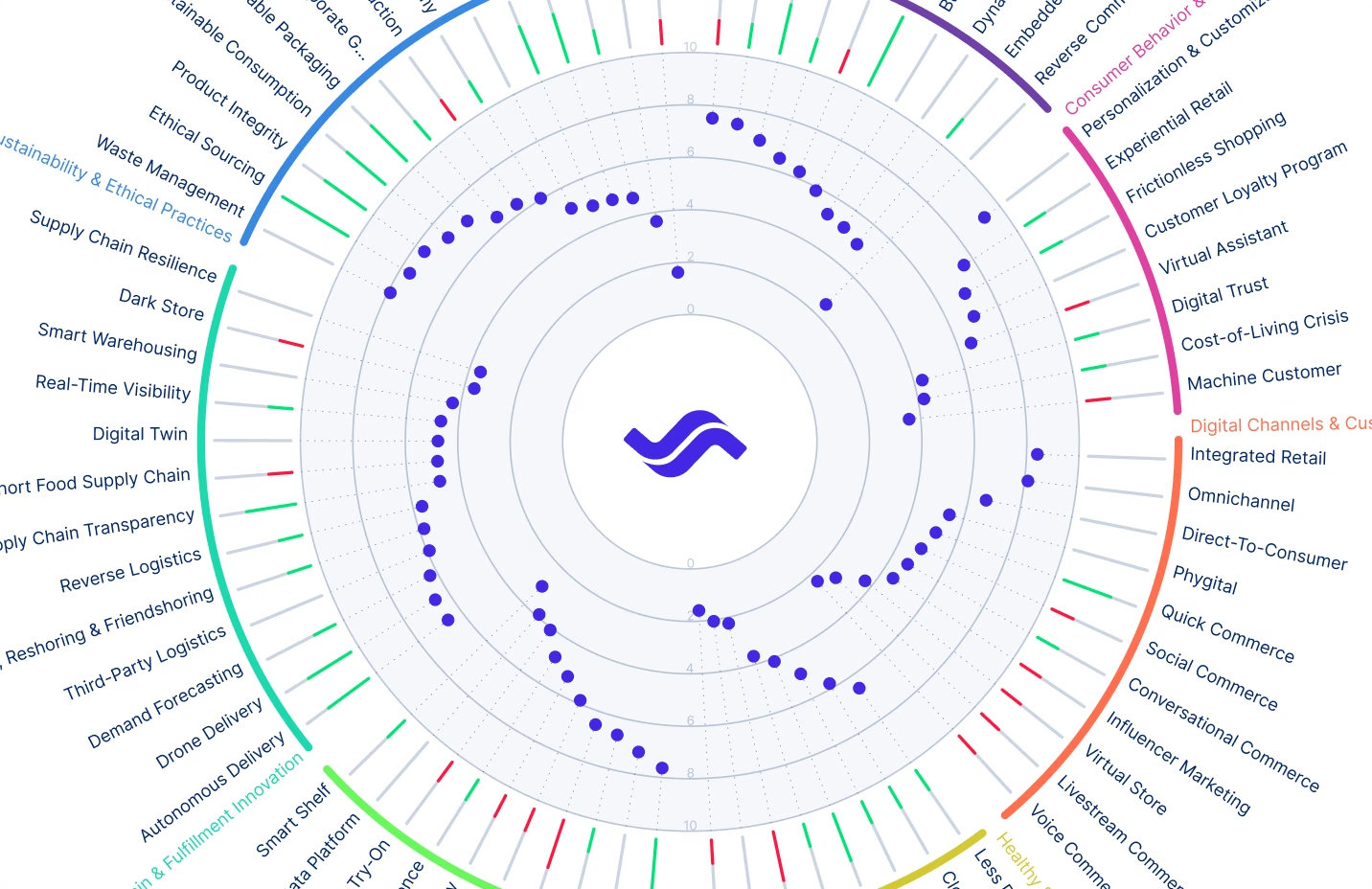

Trendtracker monitors the evolution of trends and risks continuously, scoring each on a normalised 0-10 scale by Strength and Momentum for direct comparison. Unlike general-purpose AI tools, it factors in your organisation's specific context, competitive landscape, and strategic priorities - so insights are quantified, tailored, and built on a live picture rather than a point-in-time response.