Battery Energy Storage System

15

%

8.2

The only AI-powered strategic intelligence platform that transforms global market shifts into high-impact decisions for energy leaders navigating industry disruption.

Globally, investments in battery energy storage systems (BESS) are rapidly increasing, with significant projects underway across all continents, signifying a strong commitment to enhancing grid flexibility and renewable energy integration. This trend is fueled by the need for stable and reliable power storage solutions.

Increased deployment of BESS leads to varied revenue streams and energy efficiency, directly benefiting operational efficiency through energy management systems. Initial BESS investments anticipate upstream impacts like R&D impetus and engagement with regulatory bodies for compliance with new standards. Operational efficiency is boosted with competitive energy storage systems that provide flexibility to manage renewable intermittency, reducing resource wastage and overheads

Invest in large-scale battery energy storage systems (BESS) to enhance grid stability and renewable energy integration. This action can address regulatory pressures for cleaner energy and boost operational efficiency by stabilizing energy distribution, crucial for ensuring reliable service to customers.

The AI-driven energy demand is poised to significantly impact electricity systems globally, with AI usage projected to increase energy consumption sharply in the coming years. This trend will drive demand for more advanced grid management solutions and renewable energy integration to meet this challenge.

Rising electricity demand for AI data centers increases energy production costs and necessitates infrastructure investment, impacting operational efficiency and resource management. Intensified scrutiny from regulatory authorities may result in tighter compliance requirements, affecting company flexibility and operational strategies. AI's impact on electricity consumption raises operational costs and influences investment strategies to increase grid reliability and efficiency

Explore partnerships with tech companies, such as Microsoft and Google, to integrate their innovative energy technologies into operations. This can optimize energy usage at data centers, improving energy efficiency and reducing costs, aligning with sustainability and carbon reduction goals. Invest in advanced energy storage solutions to support renewable energy integration and manage AI-driven energy demands sustainably. This addresses the economic need to stabilize electricity prices while enhancing operational efficiency, vital for competitive market expansion and energy transition.

There is a growing trend towards integrating long-duration energy storage (LDES) within industries like aluminium to stabilize renewable energy integration, thereby reducing cost volatility and increasing competitiveness in the medium to long term. Governments are increasingly supporting industrial decarbonization through financial incentives and policy changes, leading to significant investments in renewable energy infrastructure. This support is crucial in driving long-term carbon emission reductions, although short-term action might be limited by regulatory and financial barriers

Government grants and funds boost industrial decarbonization initiatives directly impacting operational contexts, reducing emissions, and stabilizing energy prices. Hydrogen integration increasingly supports decarbonization in heavy industries, directly impacting refining operations and augmenting clean energy supply. Increased reliance on renewable sources for electricity necessitates grid infrastructure modernization for effective industrial decarbonization

Invest in long-duration energy storage (LDES) technologies to secure a stable renewable energy supply, mitigating the impacts of energy price volatility and enhancing competitive positioning by reducing reliance on fossil fuels for energy-intensive processes. This aligns with sustainability goals and operational efficiency improvements.

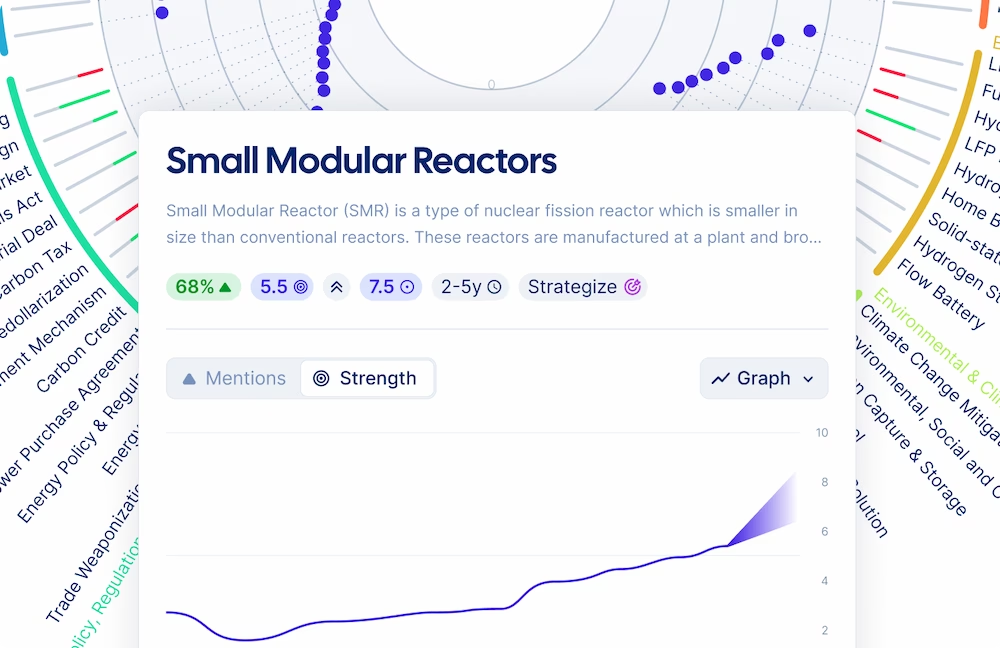

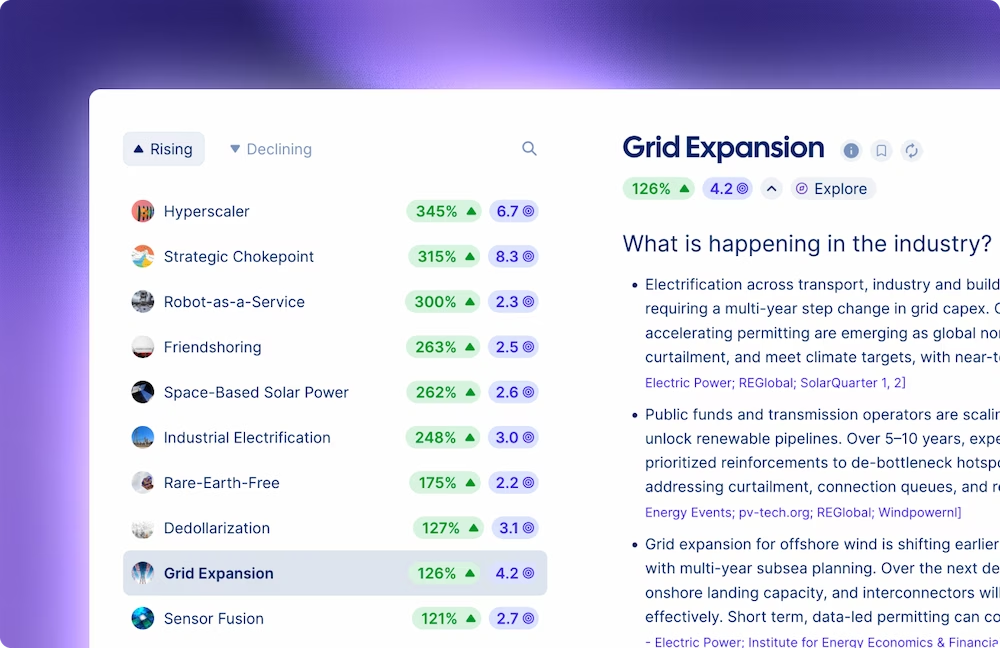

Trendtracker scores technology signals by momentum across policy, investment, technology, and regulatory sources simultaneously - revealing whether acceleration is broad-based across geographies and sectors, or concentrated in a single region or funding cycle. Energy leaders use this to separate technologies approaching commercial viability from those still dependent on policy support, before committing capital.

Yes. Trendtracker monitors geopolitical and policy signals across geographies in real time - scoring each by momentum so teams can distinguish between policy directions that are hardening into requirements and those still contested. Investment and infrastructure decisions are timed to actual signal strength, not political announcements.

Trendtracker surfaces competitor signals alongside the technology and policy trends driving them - so teams understand not just what competitors are investing in, but which signal clusters are behind those moves. This gives energy strategy teams a basis for assessing whether a competitor's move reflects a broadly accelerating trend or a first-mover bet on an early signal - a critical distinction for timing your own positioning.

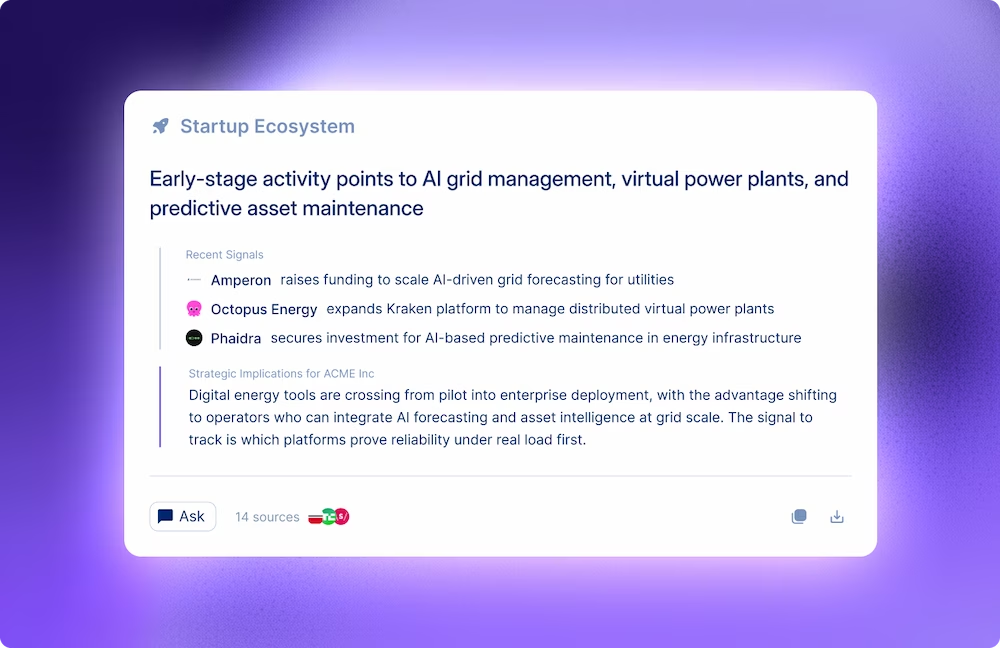

Trendtracker monitors signals across digital energy infrastructure, grid technology, AI adoption in utilities, and IoT-enabled asset management - scored by momentum and linked to the broader energy transition trends they enable. Strategy and innovation teams use it to track which digital energy technologies are moving from pilot to enterprise scale, and which industries and geographies are leading adoption, so infrastructure investment decisions are grounded in current signal evidence.

Each function operates within its own dedicated view - clean energy technology, regulatory compliance, geopolitical risk, digital infrastructure - while drawing from the same underlying intelligence. This means strategy, sustainability, and regulatory teams are always scanning the same signals, not building separate and potentially contradictory pictures of where the energy transition is heading.