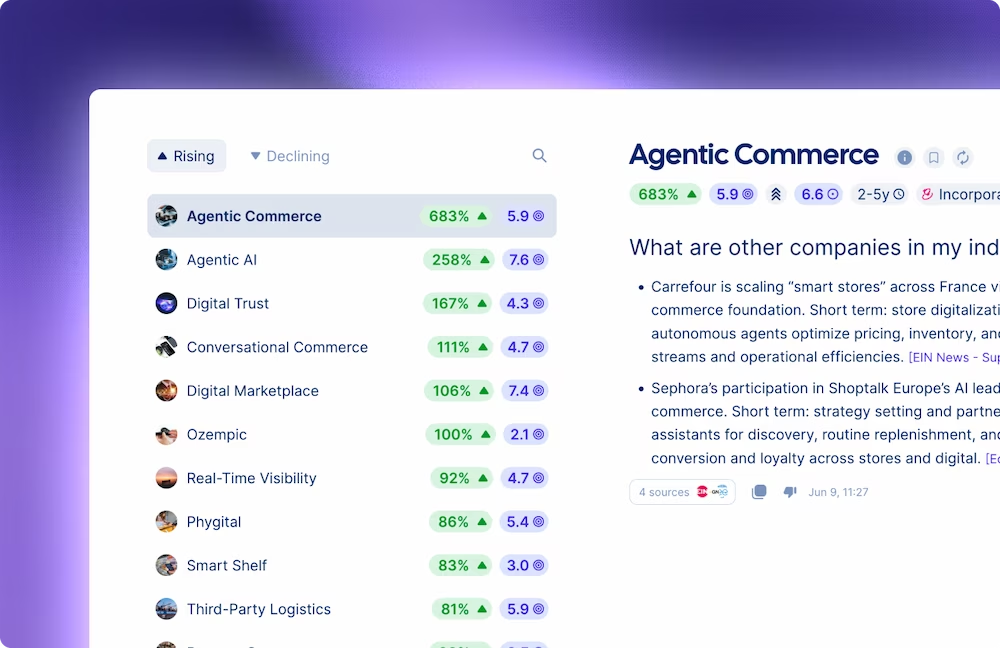

Agentic Commerce

1538

%

6.4

The only AI-powered strategic intelligence platform that transforms global market shifts into high-impact decisions for retail leaders navigating industry disruption.

Agentic commerce is set to transform retail by enabling AI agents to autonomously handle shopping, from discovering products to completing purchases, greatly enhancing customer experiences and operational efficiencies in the long-term.

The immediate advent of agentic commerce in the retail sector will lead to automation and personalization of shopping experiences, driving revenue with increased consumer engagement and streamlined operations. Retailers will see a surge in capital expenditure on AI technology. As online platforms and brick-and-mortar stores integrate AI systems, operational costs and workforce dynamics will evolve significantly.

Integrate AI-powered agents into the retail experience to anticipate customer needs and personalize shopping. This enhances convenience and satisfaction, aligning with changing consumer preferences for seamless and personalized shopping. Implement data analytics to monitor agent performance, ensuring compliance and improving customer interactions with AI technologies.

The implementation of dynamic pricing is becoming more prevalent among retailers like Walmart, Kroger, and Amazon. This strategy allows these companies to frequently adjust their prices based on market conditions and consumer behavior, potentially enhancing profit margins and inventory management.

Dynamic pricing directly impacts revenues by optimizing prices based on demand. It also influences costs due to the need for technological investment in real-time price adjustment systems and affects customer purchasing decisions by offering competitive deals. The use of dynamic pricing supports personalized and efficient shopping experiences, aligning with digital transformation and supply chain optimization strategies. Its integration can lead to improved financial performance by maximizing sales and reaching broader markets with differentiated price points.

Leverage AI-driven dynamic pricing to optimize pricing strategies, enhancing customer satisfaction and loyalty by offering competitive pricing that adapts to demand. This approach can mitigate regulatory pressures while providing data for refining promotional strategies. Balance short-term fluctuations with long-term price stability to maintain consumer trust.

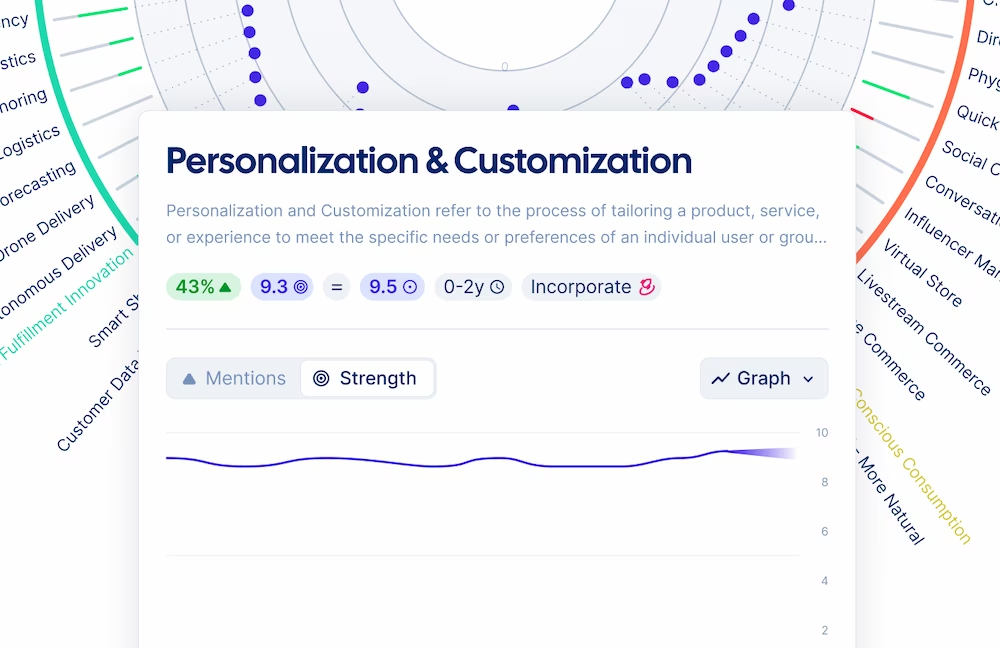

AI-driven personalization is rapidly transforming retail, offering tailored experiences that enhance customer loyalty and drive sales. This personalization leverages vast data quantities, enabling retailers to create hyper-personalized marketing and product strategies.

Retailers focusing on AI-driven hyper-personalization see improved customer engagement through tailored in-store and online experiences. These advancements directly impact purchase decisions, drive revenue growth, and boost customer satisfaction. As personalization becomes a standard expectation, retailers must navigate increased competition and data privacy concerns. Companies investing in AI-driven experiences may foster deeper customer loyalty but must balance with regulatory compliance and ethical data use.

In the short-term, focus on integrating AI-driven personalization tools to enhance customer experiences by creating hyper-personalized engagement based on real-time data. This can improve customer satisfaction and boost sales. In the medium to long-term, expand the use of advanced analytics to deepen customer insights and refine product offerings, addressing technological advances and social consumer trends towards personalized experiences

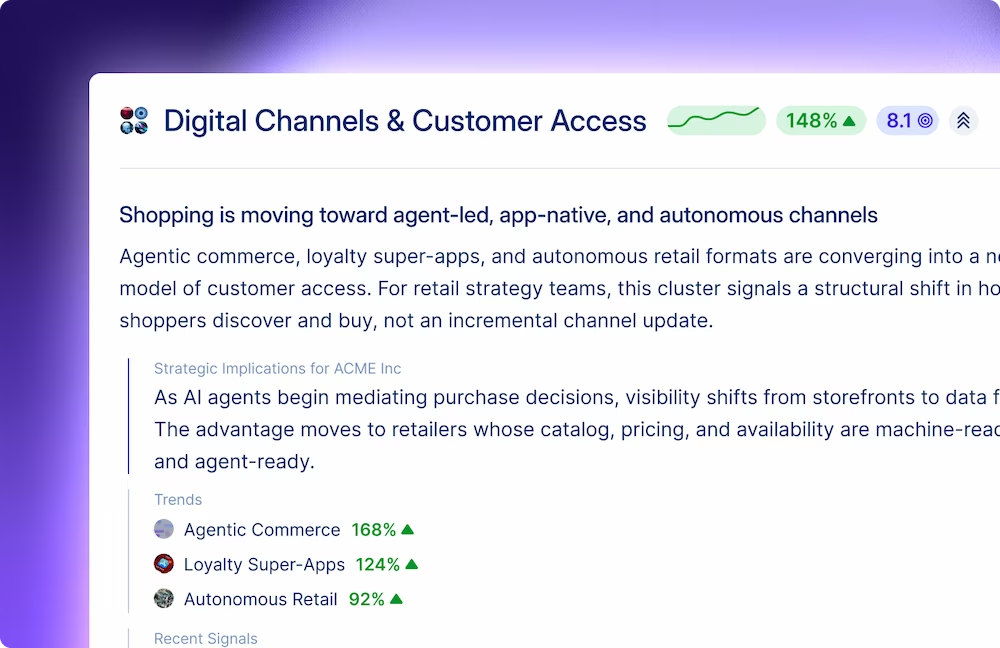

Trendtracker monitors signals across consumer sentiment, digital commerce, social commerce, and retail format innovation in real time - scoring each trend by momentum. Your strategy team gets early visibility into which behavioral shifts are gaining traction across geographies and demographics, so planning decisions are based on where the consumer is going, not where the data currently shows they are.

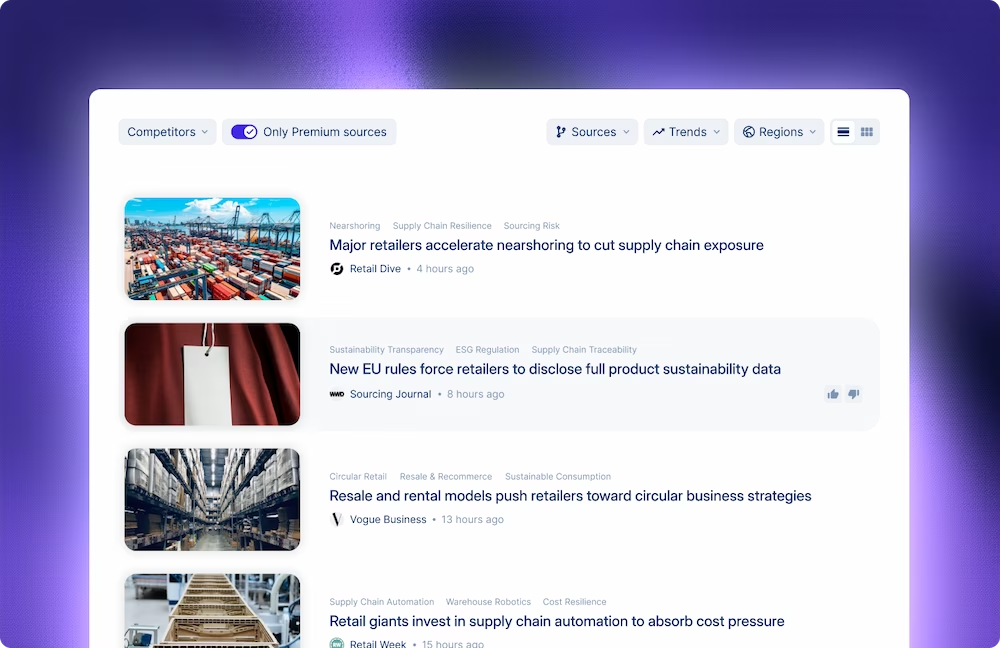

Yes. This is one of the core use cases for retail teams. Trendtracker monitors signals across geopolitical risk, logistics disruption, nearshoring trends, and commodity price movements - ranked by strategic relevance. Procurement and operations teams use it to anticipate where supply chain pressure is building before it hits lead times, and to identify which nearshoring or supplier diversification moves competitors and adjacent industries are making.

Trendtracker tracks adoption signals for emerging retail models across the full signal landscape - from startup activity and platform investment to consumer adoption data and regulatory signals. Teams configure Trend Boards around the specific models most relevant to their strategy, so they see which formats are gaining momentum across markets and which are still experimental - before making format or channel investment decisions.

Trendtracker monitors signals across sustainability regulation, consumer transparency expectations, circular economy adoption, and ESG disclosure requirements - scored and ranked by momentum and geographic relevance. Retail strategy teams use it to track which sustainability expectations are hardening into regulatory requirements and which are still consumer preference signals, so sustainability investments are timed and targeted correctly.

Yes. Trendtracker's shared Trend Boards allow different teams to work from the same signal intelligence, with access controls and parallel boards by category or domain. This means strategy, merchandising, and supply chain teams are scanning the same landscape rather than building separate and potentially contradictory views of where the market is heading - a common source of misalignment in large retail organisations.