AI-Driven Drug Discovery

78

%

6.4

AI-driven drug discovery is experiencing accelerated growth with significant investments and collaborations among industry leaders. These partnerships aim to reduce drug development timelines and costs, indicating a rising trend likely to sustain long-term impact.

AI in drug discovery boosts speed and cost efficiency, reshaping R&D investments and timelines. Companies notice immediate impacts in the drug pipeline and operational costs, resulting in efficiencies. AI developments change competitive dynamics, prompting regulatory adaptations and focus on digital innovation. Companies increasingly face pressure to integrate robust AI systems, affecting investment strategies towards AI infrastructure.

Form strategic partnerships with AI companies to boost R&D in drug development, focus on reducing time and cost, and enhance AI integration for precision medicine. Collaborations with tech giants can accelerate innovation, meet regulatory demands, and improve market access, leading to more effective patient-centric treatments.

The pharmaceutical industry's focus on digital transformation, such as using AI and RFID technology, is crucial for enhancing supply chain resilience. This improves risk management and operational efficiency, strengthening the industry's ability to adapt to disruptions.

Diversification of supply sources and collaborations with local facilities can immediately stabilize raw material availability and reduce the risk of interruptions, directly impacting manufacturing efficiency and cost management. Strengthened supplier relationships and enhanced supply chain resilience contribute to long-term competitive advantages, affecting market dynamics, customer satisfaction, and regulatory confidence in pharmaceutical products

Pharmaceutical companies could advance supply chain resilience by investing in domestic manufacturing, reducing dependency on foreign suppliers, and enhancing FDA compliance. This could ensure drug quality and availability, aligning with regulatory demands and supporting operational efficiency. Governments and investors may favorably view this proactive resilience building.

Precision medicine is transforming drug development, enabling more accurate treatment options through integrating biomarkers and genetic data. This shift can lead to improved patient stratification, offering tailored therapies that enhance treatment efficacy and safety, ultimately reshaping pharmaceutical strategies.

The shift to precision medicine leads to targeted therapies, improving drug efficacy and reducing adverse effects. This can optimize the drug approval process, shortening time to market and enhancing revenues from innovative products. Precision medicine's personalized treatments increase R&D costs but promise better patient outcomes, leading to enhanced trust from healthcare providers and patients. This also attracts more investment due to potential breakthroughs in chronic disease management.

Leverage biomarkers to accelerate precision medicine in R&D. By integrating robust biomarker strategies in drug development, the company can enhance patient stratification and tailor effective therapies, optimizing both patient outcomes and regulatory compliance. This aids R&D excellence and supports efficient market expansion

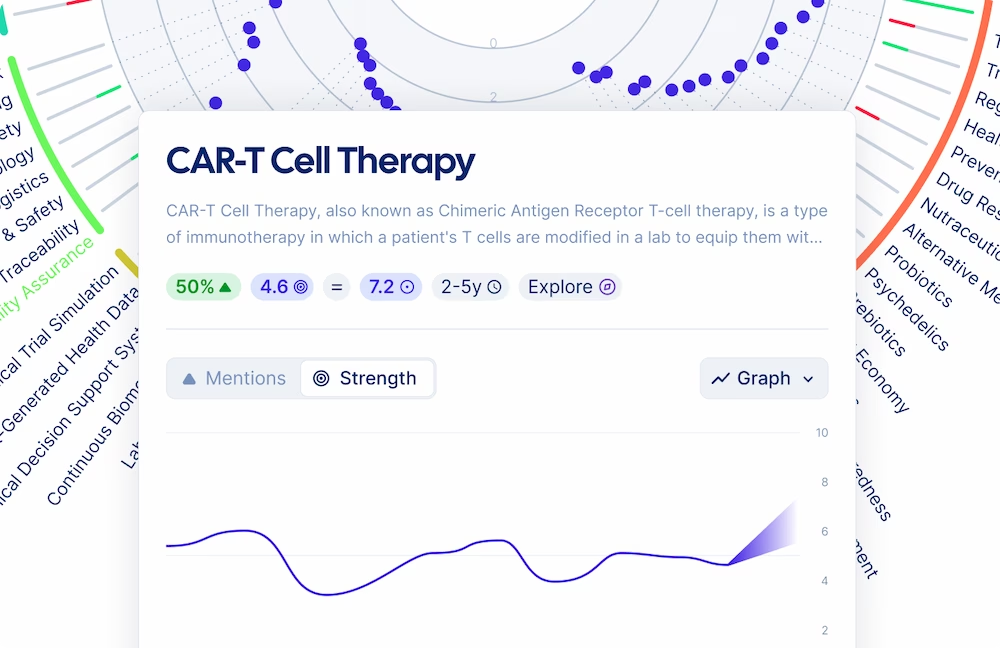

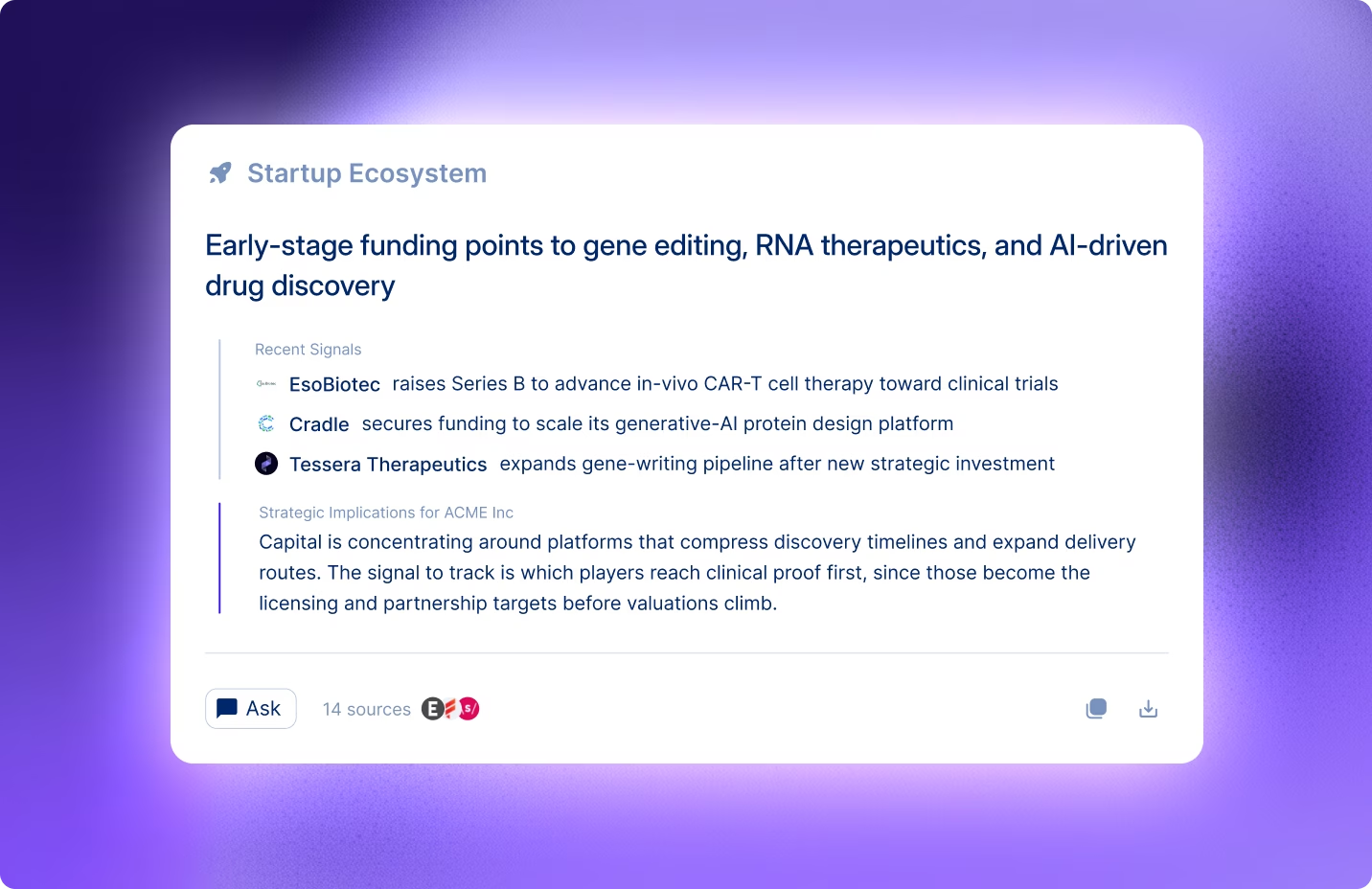

Trendtracker continuously monitors patents, peer-reviewed research, venture funding, and M&A activity across {{sources}}+ curated sources. Insights are traceable to the underlying sources, so findings can be verified and shared with confidence. This gives R&D and strategy teams early visibility into where scientific momentum is building and where investment is concentrating, before those signals reach mainstream analyst coverage.

Trendtracker is designed to recognize the specific terminology used in life sciences as they appear across scientific literature, patents, regulatory filings, and investment data - so trend scores reflect the complete picture of activity, not a partial one.

Most existing tools deliver depth at a point in time. Trendtracker adds what sits between those reports - a continuously updated intelligence layer that scores each trend by Strength and Momentum on a normalised scale, so signals are always directly comparable without manual effort. Teams spend less time maintaining the process and more time acting on what it surfaces.

Trendtracker surfaces competitor activity alongside the scientific and regulatory shifts behind it - so teams see not just what a competitor is developing, but which broader move they may be responding to. It also brings less obvious competitors into view from adjacent areas, helping teams judge whether a pipeline move points to a wider therapeutic shift or an isolated bet before committing to a position.

Yes. Different teams across the organisation work from the same continuously updated intelligence, each focused on the trends and domains relevant to their function. This makes trend intelligence a shared reference point rather than a set of parallel analyses running in isolation - reducing duplication and keeping every function aligned on the same evolving picture.